It is December now and the winter is making things cool.

But it is the time to think beyond ‘Roses in December’. The reason is obvious. Administration departments are shooting off notices and mails to the employees to submit their investment proofs for tax computation purpose.

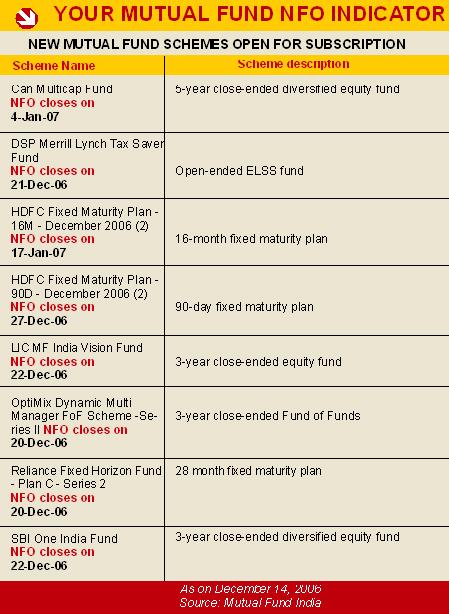

A couple of mutual fund houses have launched tax saving schemes and the others already having one, have opted to advertise them. Tax planners and investment consultants are gearing up for the ‘season’ and the taxpayer as usual are trying to ascertain where they stand.

Taxation simplified

Tax -- a payment to state ‘in absence of quid pro quo’ means without anything in exchange -- is certainly not a welcome phenomenon in life. Income tax, also known as the king of direct tax, is no exception to this.

Nowadays tax planning is the unwanted reality that everyone has to confront. Saving on tax need not be an expert’s forte, though the experts can come out with better strategies. For assessees with less income, tax issues are manageable on their own.

Tax planning starts with understanding one’s tax liability. Computation of gross taxable income and arriving at the net taxable income after providing for all deductions is not rocket science. For tax rates and the process of computation of tax liability refer to the tables attached herewith.

Tax rates are high in India and ensure that the income tax is a tax of progressive nature. The highest marginal rate of income tax is 30% for individuals. It is further enhanced by the treatment of surcharge and education cess. Education cess is payable by all assessees and on the other hand the surcharge is payable by only those who have an income in excess of Rs 10,00,000 after adjusting for all the available deductions.

Instruments of investments

On the back of the sustained rise in the equity markets, equity linked saving scheme (ELSS) became the most sought after investment vehicle along with ULIPs offered by the insurance companies. The debt instruments like PPF, NSC have taken a back seat. One should carefully examine what the approved vehicles bouquet is all about?

Provident fund (PF) and public provident fund (PPF) are the ‘social security twins’ that qualify for deduction under section 80C. PPF and PF are the oldest options in the tax saving-investment basket for Indian investors and offer least complexity in operations along with near certain returns. Maximum Rs 1 lakh contributed to PF and PPF qualifies for deduction under this section.

Both PF and PPF are predominantly being seen as social security solutions offering less liquidity. PF is a vehicle accessible by the salaried class and managed through the employer. On the other hand, PPF is meant for both salaried and non-salaried strata of society and can be maintained with selective banks and post offices. The biggest positive of PPF is that the proceeds from a PPF account cannot be attached in any circumstances, making it an investment for ‘tough times’.

National Saving Certificate (NSC) comes with a term of six years. The government decides the rate of interest and it is equivalent to sovereign obligation, depicting low risk.

For assesses who are in the last leg of their working life, these avenues along with NSC issued by post offices offer great value. Less risk along with assured returns makes it a worthy investment proposition for these investors.

Life insurance premium paid up to Rs 100,000 also qualify for the deductions under section 80C. Earlier, barring few, tax rebate was ‘the reason’ why one would buy a life insurance product in India. The endowment plans typically were bought for the tax rebate they offered. But things are changing now.

The ULIP bandwagon has caught up and now contributes almost 50 to 60% of the insurance companies’ premium income. However, there are some inherent risks an investor should take cognisance of.

Since the last three years Indian equity markets are booming on the back of structural growth. By default, the money invested into ULIP enjoyed highest possible allocation to equity, in most cases, as high as 100% of allocable funds. However, one should understand the risk accompanied with such returns.

Though ULIP as per revised guidelines, come with at least three years lock-in, ensure the long-term participation across asset classes, the focus on equity makes it a product meant for investors with higher risk appetite. However, one should choose a rational mix of debt and equity depending upon one’s risk appetite and investment goals. A 100% allocation to equity may not be a suitable option for a person who is in the last few years of working life and is sitting on a good amount of accumulated savings.

However, young tax payers can look at this option for long-term wealth creation. One should be careful while choosing a ULIP. The allocation percentage and the fees charged under various heads should be carefully studied.

There are many single premium options available with high allocation and low charges options in the market. Such single premium options along with top up facility offer great value to the investor in the long term. To ensure that the money made by them will be protected in corrective phases in the markets, savvy investors can use free switches between debt and equity.

In the young age, insurance may not be popular. Along with cost effective fund management, the insurance cover is a further value enhancer.

The life insurance premium is not just restricted to ULIP and endowment plans, the cheap term insurance products is another avenue that can be considered. These products are useful, especially to the young investors, who aspire for the best lifestyle and leverage themselves financially to achieve these goals. Also in the younger age, the level term products are available at throwaway prices in view of good mortality and insurability of lives.

Equity linked saving schemes of the mutual funds allow an investor to ride the boom in the stock market. Systematic investment plans (SIP) is the best option to take exposure to this instrument. Schemes with longer track records should be given preference.

If one has not invested in such schemes till date, exposure in small lots over the next three months is a better strategy as it may avoid the possibility of all investment at the top. Also, before investing in any scheme of a mutual fund, one must check if it offers deduction under section 80C and investing in an ELSS is not a universal recommendation.

Fixed deposits with banks also qualify for tax rebate. Most of the banks have come up with such products, having minimum term of five years. They offer stable returns with less risk.

Contribution to pension schemes up to maximum of Rs 10,000 is deductible under section 80CCC. However, this amount is not in addition to the 80C deductions discussed earlier. In other words, a person who has invested Rs 1 lakh in instruments qualifying for deduction under section 80C and invested Rs 10,000 in an approved pension fund under section 80CCC, will get total deduction of Rs 1 lakh only.

This is a good investment, taking into account the lack of adequate social security in our society. Especially for those who are self-employed or do not have a pension benefit from their employers, this avenue offers unmatched value.

Housing loan repayment also qualifies for deduction. The repayment of housing loan principal qualifies for rebate under section 80C. Pre-payment of housing loan also qualifies for the deduction. The interest payable on the housing loan is deductible under section 24. The maximum amount of interest that can be deductible is Rs 1.5 lakh.

Housing is an important need of a human being. With the tax-sops attached with housing loan, it offers immense value to the borrowers. Housing loans can be used to effectively plan one’s tax liability.

Housing loans come with the lowest rate of interest compared to other loan products in the market. A tax deduction reduces the real cost of borrowing to the tune of 30% (assuming the taxpayer is in the highest tax bracket).

A person, who is in the initial years of the housing loan, can opt for lump sum repayment of loan in addition to his equated monthly instalments (EMI). In the initial EMIs the principal component is less compared to interest component. The additional lump sum paid along with principal component paid through EMI qualifies for tax deduction to the maximum of Rs 1 lakh.

This repayment allows the individuals to reduce their loan tenures and also become debt-free at the earliest along with the tax benefits. In addition to the loan payment the individual escape investing in various instruments to avail of tax break, straining the cash flows. Also, it leads to creation of an asset in the long term and with the booming real estate market making it a further more attractive ‘investment’.

However, before resorting to repayment, the borrowers should ascertain the principal and interest components in the equated monthly instalments they will be paying in the financial year. This is readily available in the provisional loan repayment statement provided by the banks at the start of the year. Accordingly, one must ascertain the extent of repayment he can go for. Also the prepayment charges, if any, should be taken into account while going for the prepayment.

The premium paid for medical insurance plans attracts deduction under section 80D to the maximum amount of Rs 10,000. This is not an investment product and does not offer any maturity value, it is equally important with other tax saving avenues. Health insurance is the need of the hour and will be felt today or tomorrow by everybody. Equity markets and real estate markets have done extremely well, and people have made good returns on their investments. Short-term capital gains attract 10% short-term capital gains tax. Long-term capital gains is another area where investors have to pay more attention.

There is no tax on long-term capital gain on the sale of shares of companies listed on the stock exchanges. However, sale of land and other assets such as house attracts long-term capital gains tax. One can invest in approved bonds under section 54EC to get rid of this tax.

However, as there is no such issue that is going on, it is time to wait and watch for the next bond issue to that effect.

If you are still left with income tax liability after exhausting all the possible options to avoid tax, then better pay the tax than evade it. The next thing to remember is payment of advance tax. The two dates of payment of advance tax falls on December 15 and March 15, for those whom advance tax is applicable.

Income tax, though not a welcome phenomenon, certainly is not as haunting as it appears to be. One should take advantage of all these instruments and just not avoid the tax liability but also take the provisions to one’s own advantage.

to know how to invest for tax purpose write to

personalfin@gmail.com